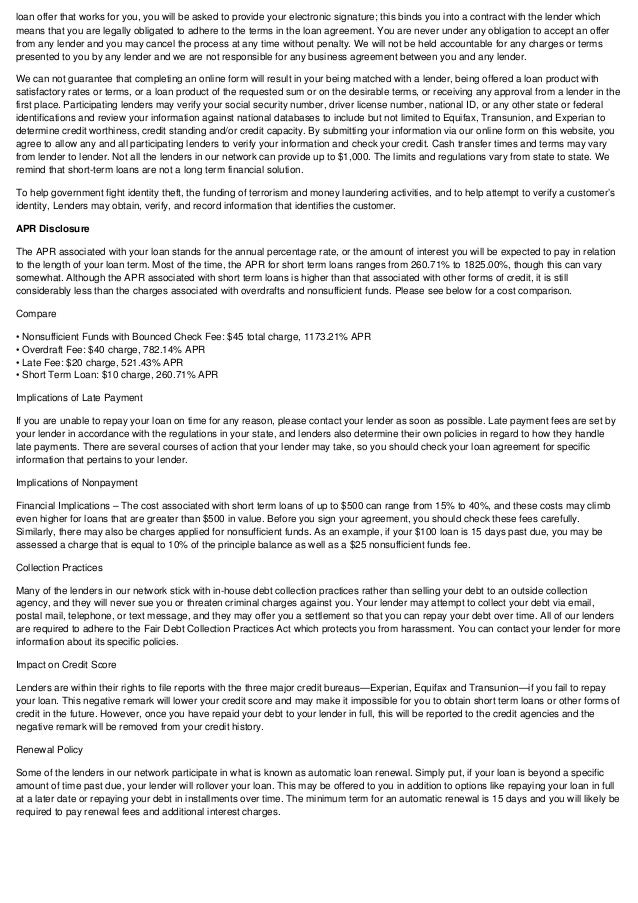

Given that rates , loan providers who generate mortgage brokers in order to Tx owners was viewing an uptick in the loan modification requests. In the event good mod to possess a conventional financing is straightforward, there are bear in mind unique pressures with respect to home equity loans. This article will explore certain key factors Texas loan providers might want to take on whenever navigating these changes.

Do our home guarantee financing law apply to good mod?

Sure, your house guarantee credit law and Interpretations (regulations) have a tendency to still apply. The new guidelines claim that our home guarantee requirements out of Section 50(a)(6) could well be used on the initial financing therefore the further amendment given that just one deal. This might be each other bad and the good. New restrictions on the household equity loans pertain, but the majority lenders should be able to fit the Pine Level pay day loan expected improvement within present loan program. Subsequently, this could allow brief and you may cheap getting loan providers and make mortgage mods one just change the applicable interest.

Exactly what changes are allowed?

The lending company and borrower is also agree to create, erase, or tailor people financing supply as long the changes was agreeable on the Colorado household security statute and laws and regulations. Brand new statutes declare that a modification of an equity mortgage might not provide for this new terms and conditions who not have started allowed from the relevant law on the latest day out of closure of your extension from credit. Particularly, there is no limitation (besides the latest usury limit) with the rate of interest, and is one fixed or varying interest licensed significantly less than statute. Simultaneously, the borrowed funds cannot be restructured to have an effective balloon percentage, that’s blocked from the Constitutional supply that really needs the loan to get arranged getting reduced for the substantially equal successive occasional installment payments. So it requirements is much more complicated to possess a property equity type of borrowing from the bank, and this must take into account brand new draw several months along with new cost period.

Can also be the new borrower consult a beneficial mod by cell phone otherwise on line?

Sure, brand new debtor makes new consult because of the cellular phone, on the internet, or in person, nevertheless the real amendment contract must be in writing and you may finalized from the bank and you will borrower. Some exclusions get deployed military group or any other some body.

Normally the new borrower rating an effective mod inside a-year immediately after its last domestic equity mortgage?

As the lenders discover, a debtor never personal an alternate domestic guarantee loan within one season immediately following obtaining an earlier domestic guarantee loan, with the exception of a proclaimed state away from crisis. That it rule does not affect loan mods. A house guarantee loan modification can be made during the twelve-times several months.

Is actually a cooling off several months necessary?

In lieu of the first family equity mortgage, there is not an air conditioning-out-of period before financing mod is personal. And additionally, the newest debtor doesn’t always have a straight to rescind the newest amendment agreement. Given that notice isnt changed, and deed away from trust was (usually) unchanged, the newest lien into property is continuingly valid plus the finance can be paid towards the borrower instantaneously.

Can also be the new debtor get a lot more money?

Probably one of the most tricky regions of property equity loan amendment is determining what wide variety are permitted while the the latest principal balance. New borrower you should never disappear throughout the dining table with any additional funds, however the financial must also imagine whether and how to capitalize outstanding prominent and you can notice, taxes, and you may insurance premiums, and you will whether to account for PMI visibility and other products. Adjustment into the action off faith present unique considerations which go past family guarantee lending things and want the assistance of a beneficial competent a property attorney in many cases.

Normally brand new borrower get out of your house equity loan entirely?

As loan providers know, a property equity loan should be turned into a normal financing by following the specific criteria regarding the Colorado Structure. Although not, eg a purchase would not qualify because an amendment. It is noticed an effective re-finance.

Sure, but bear in mind one given that regulator usually lose the modern loan as well as the mod as one purchase, the 2% cover for the fees commonly incorporate. Together with, in the event your lender has identity insurance rates, new term organization, more often than not, often ask you for for modifying otherwise updating the policy. Likewise, most other will cost you which can be excluded from the 2% cover, like a name lookup otherwise survey, really should not be expected. The lending company may want to get a new appraisal in a few products. Generally, a loan mod should be pricing-productive towards lender and also the borrower. The procedure should be temporary and only just like the challenging while the it should be.

For Colorado lenders navigating the causes of family guarantee mortgage changes, McGlinchey’s experienced cluster is actually really-trained on the certain pressures these changes establish and can provide tailored advice to ensure compliance having Colorado rules. When you have issues, excite get in touch with the author otherwise McGlinchey’s Home loan Lending Compliance party.